The Complete Guide to White-Label Wealth Management Platforms

A white-label wealth management platform is licensed infrastructure that an independent wealth manager, multi-family office, or trust company operates under its own brand. The platform provides portfolio management, client reporting, compliance, trading, and onboarding capabilities without the firm building or maintaining the underlying technology. White-label deployment typically takes weeks rather than the 12-18 months required for custom development.

Contents

- What Is a White-Label Wealth Management Platform?

- Why Wealth Managers Are Moving to White-Label Platforms

- White-Label vs Custom Build vs Generic Software

- Seven Evaluation Criteria for Platform Selection

- How Do Wealth Managers Use White-Label Platforms in Practice?

- Cost Analysis: What Wealth Management Software Actually Costs

- Common Concerns About White-Label Platforms

- How Aerapass Works as a White-Label Wealth Platform

- Frequently Asked Questions

What Is a White-Label Wealth Management Platform?

In short, a white-label wealth management platform is technology infrastructure built by one company and operated by another under its own brand. The wealth manager’s clients see the firm’s name, logo, and domain. The platform provider remains invisible.

This model has existed in financial services for decades - payment processing, card issuance, and custody services have long operated on a white-label basis. What has changed is the scope. Modern wealth management SaaS platforms now cover the full client lifecycle: digital onboarding, KYC/AML screening, portfolio construction, rebalancing, multi-asset trading, consolidated reporting, and regulatory compliance across jurisdictions.

The distinction from generic wealth management software matters. Off-the-shelf software provides tools that carry the vendor’s brand, interface patterns, and workflow assumptions. A white-label platform provides the same capabilities but with complete brand ownership - the client experience belongs to the wealth manager, not the technology provider.

Three deployment models exist in the market:

Fully hosted. The platform provider manages all infrastructure, security, and updates. The wealth manager configures the platform, adds clients, and operates under its brand. This is the fastest deployment path and the most common model for firms with fewer than 50 employees.

Hybrid. The wealth manager hosts certain components (typically the client-facing portal and data storage) while the platform provider manages the core infrastructure, compliance engines, and trading connectivity. This model suits firms with specific data residency requirements or existing technology investments.

API-first modular. The wealth manager integrates individual platform modules - portfolio management, reporting, compliance - into its existing technology stack via APIs. Each module operates independently. This model requires internal engineering capacity but provides maximum architectural flexibility.

Why Wealth Managers Are Moving to White-Label Platforms

The wealth management industry is undergoing a technology transition driven by three forces that make the status quo unsustainable.

Client expectations have permanently changed. Capgemini’s 2025 World Wealth Report found that 44% of wealth managers still operate on outdated platforms, while 25% of high-net-worth investors would consider switching firms over inadequate digital experiences. The gap between client expectations and platform capability is widening, not closing. Bain’s 2024 wealth management study found that personalized digital experiences drive 20-30% higher client retention - making platform quality a direct driver of revenue retention.

The asset class landscape is expanding. Tokenized securities, fractional real estate, digital assets, and structured products are moving from experimental to expected. The real-world asset (RWA) tokenization market reached $18-33 billion in 2025 according to BCG and Ripple, with projections of $18.9 trillion by 2033. A platform that cannot support multi-asset classes within three years is a platform that needs replacing.

Regulatory complexity is accelerating. MiCA took full effect in December 2024. The GENIUS Act passed in the US in July 2025. MAS continuously updates its Payment Services Act. Each regulatory change requires technology adaptation. For firms managing client portfolios across borders, maintaining compliance infrastructure internally has become prohibitively expensive.

The global wealth management platform market reflects this urgency, growing at 10.6% annually and projected to reach $11.5 billion by 2028 according to Grand View Research (2024).

White-Label vs Custom Build vs Generic Software

The key difference is who owns the technology, who owns the brand, and who bears the operational burden. This comparison table covers the six dimensions that most frequently determine the decision.

| Dimension | White-Label Platform | Custom Build | Generic SaaS |

|---|---|---|---|

| Time to launch | 2-8 weeks (configuration and branding) | 12-18 months to MVP | 1-4 weeks (onboarding to vendor's system) |

| Branding control | Full: client-facing portal, reports, communications all carry the firm's brand | Full: everything is purpose-built | Partial: vendor branding visible in interface, reports, login screens |

| Compliance coverage | Varies widely. Some providers offer compliance tooling only; others hold their own regulatory licenses. Confirm whether the provider is licensed or simply providing technology that requires the firm to obtain its own licenses | Self-managed per jurisdiction. $100K-$300K and 3-6 months per market | Basic compliance tools. Firm responsible for jurisdiction-specific requirements |

| Multi-asset support | Most platforms cover traditional securities and alternatives. Native support for digital assets, FX, and commodities varies significantly between providers - evaluate each platform's actual asset class coverage | Depends on build scope. Adding asset classes post-launch costs $200K-$500K each | Typically limited to traditional securities. Digital asset support rare or add-on |

| 3-year total cost | Varies by provider: subscription-based, AUM-based, fixed, or transaction-based pricing. Generally lower than custom builds but higher than generic SaaS | $2M-$5M+ (development + maintenance + compliance + security) | $150K-$400K (subscriptions + integrations). Lowest cost but lowest capability |

| Customization depth | API-first platforms: high. Monolithic platforms: limited to configuration | Unlimited (within engineering capacity) | Limited to vendor's configuration options. Workflow changes require vendor roadmap |

Sources: Oliver Wyman wealth technology analysis (2026), Emerline custom platform cost benchmarks (2026), Aerapass deployment data

The choice depends on the firm’s competitive positioning. If the firm’s differentiation is in its technology - proprietary algorithms, unique risk models, novel execution strategies - custom development may be justified. If the firm’s differentiation is in its client relationships, investment expertise, or market access, a white-label platform delivers the technology foundation faster and at lower cost so the firm can focus on what actually differentiates it.

Seven Evaluation Criteria for Platform Selection

When evaluating a wealth management platform, these seven criteria separate platforms that will support growth from platforms that will need replacing within three years.

1. Multi-asset architecture. The platform should support traditional securities, fixed income, and alternatives at minimum. If your clients require digital assets, FX, or commodities, confirm that the platform supports these natively rather than through bolt-on integrations - most white-label wealth platforms still focus on traditional and alternative assets only. Native multi-asset support across traditional and digital asset classes is a differentiator, not a baseline.

2. Regulatory coverage by jurisdiction. This is where white-label platforms diverge most. Some providers are regulated entities that hold their own licenses - the firm operates under the provider’s regulatory umbrella. Others provide technology only, leaving the firm to obtain and maintain its own licenses in every jurisdiction it serves. The distinction matters: the Synapse Financial Technologies collapse in 2024 demonstrated the risks of partnership-based regulatory coverage where no single entity owned the compliance obligation. Ask directly: “Are you licensed, or are we licensing through a partner?”

3. Client portal and reporting. The client-facing experience defines how professional the firm appears. Evaluate: real-time portfolio views, consolidated multi-custodian reporting, mobile-responsive design, downloadable reports in client-branded formats, and multi-language support for international clients.

4. API-first architecture. This determines long-term flexibility. Documented, versioned APIs allow the firm to integrate best-in-class components (CRM, financial planning tools, market data) without vendor dependency. Monolithic platforms that require all functionality to come from a single provider create lock-in risk.

5. Onboarding and KYC/AML pipeline. Digital client onboarding with integrated identity verification, sanctions screening, and PEP checks reduces acquisition cost and client friction. The critical distinction: buy the verification tools, but ensure the approval logic (who gets approved, escalated, or rejected) can be configured by the firm. Risk appetite is a business decision, not a vendor default.

6. Data portability and exit strategy. Before signing, confirm that all client data, transaction history, and compliance records are exportable in standard formats at any time. Under the EU’s Digital Operational Resilience Act (DORA), contractual exit strategies are now legally required for regulated entities. This should be a baseline expectation regardless of jurisdiction.

7. Deployment model and support. Understand what “white-label” means operationally: Is the platform fully hosted, hybrid, or API-only? What level of integration support is provided? What is the SLA for uptime and incident response? A platform with a 99.9% uptime guarantee and dedicated integration support is operationally different from one that provides documentation and a support ticket queue.

How Do Wealth Managers Use White-Label Platforms in Practice?

-

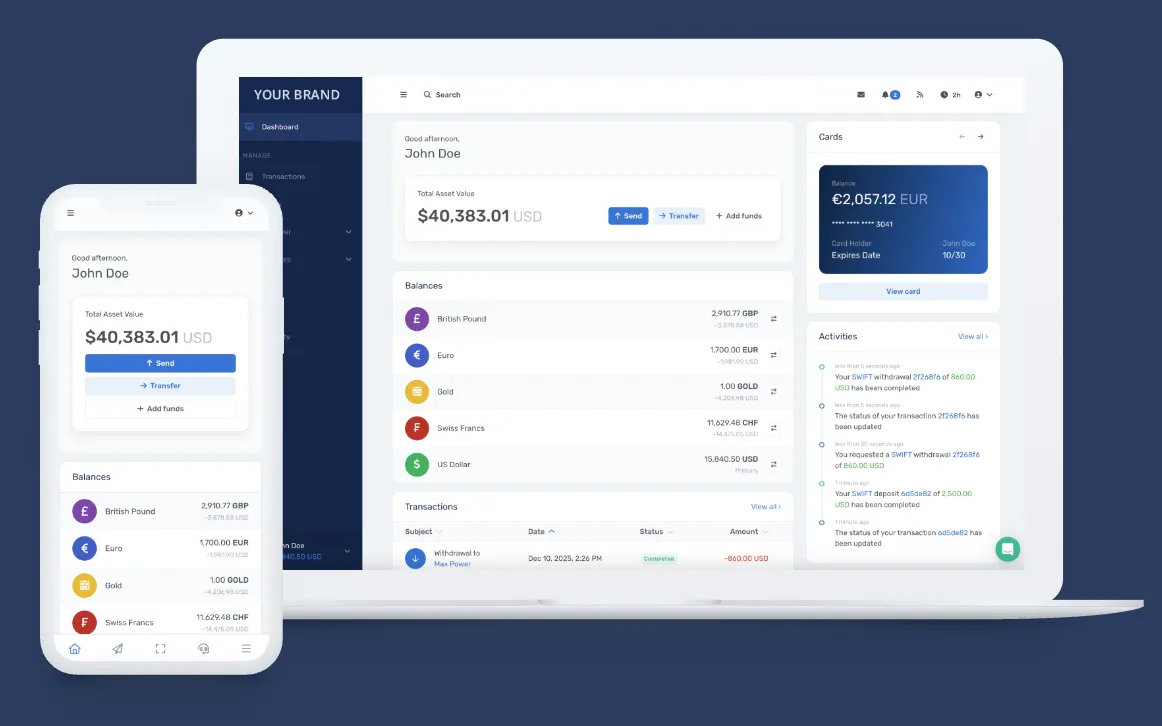

Independent wealth manager launching a branded client portal - An IWM with 200+ clients needs a professional digital experience under its own domain but lacks the 8-15 engineers required for custom development. A white-label deployment provides portfolio reporting, consolidated multi-custodian views, and downloadable client-branded statements - all carrying the firm’s identity from day one, with the platform provider managing infrastructure, security, and updates behind the scenes.

-

Multi-family office managing cross-border clients - A family office serving clients across Singapore, Switzerland, and Australia needs multi-currency settlement in CHF, SGD, USD, and AUD with consolidated reporting across jurisdictions. The global payments module handles cross-border settlement, while the wealth management platform provides unified portfolio views across all currencies and entities - without the firm building separate infrastructure for each market.

-

Trust company automating client onboarding - A corporate trustee onboarding individual, business, and trust clients faces different KYC requirements for each structure. Aerapass’s customer management module automates onboarding across all three tiers: individuals verified in 2-5 minutes, businesses in 5-15 minutes, and trust structures in 10-20 minutes. The configurable approval workflows allow the trust company to set its own risk appetite rather than accepting a vendor’s default.

-

Corporate trustee offering digital assets alongside traditional portfolios - A trustee responding to client demand for crypto and tokenized securities needs a platform that supports both asset classes without running separate systems. The multi-asset architecture handles traditional securities, digital assets, tokenized securities, and fractional ownership instruments within a single portfolio view, consolidated reporting structure, and compliance framework.

-

CRJ Capital Partners selecting platform infrastructure - CRJ Capital Partners selected Aerapass as their technology platform for wealth management operations, moving from evaluation to deployment in weeks. The firm retained full control of its investment strategy and client relationships while Aerapass provided the licensed infrastructure across multiple jurisdictions.

A white-label deployment in practice: the wealth manager’s clients see only the firm’s brand while the platform handles multi-currency balances, card management, and real-time transaction monitoring.

Cost Analysis: What Wealth Management Software Actually Costs

The most common mistake in platform evaluation is comparing year-one license fees. The total cost of ownership over three years reveals a fundamentally different picture.

Custom builds front-load cost: $2M-$5M+ over three years including development, compliance maintenance, security certification (SOC 2, ISO 27001), and engineering team retention. Hidden costs account for 40-60% of the total - regulatory update engineering, security patching, and infrastructure scaling are systematically underestimated in initial proposals.

Generic SaaS minimizes cost but also minimizes capability and brand control. At $150K-$400K over three years, it works for small firms with simple requirements and no brand differentiation needs.

White-label platforms sit between these extremes, but pricing models vary significantly across providers. Some charge subscription fees, others use AUM-based pricing (a percentage of assets on the platform), and others use fixed monthly fees. A smaller number - including Aerapass - use transaction-based pricing that scales with the firm’s actual business volume, aligning infrastructure costs to revenue rather than capacity. The economic advantage of any white-label model compounds over time: regulatory updates, security patches, and feature releases are distributed across the provider’s client base rather than borne by a single firm. Pricing structures vary by firm size and operational complexity, so the right comparison requires a tailored analysis rather than published rate cards.

For firms managing under $5 billion in AUA, the economics consistently favor private-label deployment over custom builds. Above that threshold, custom development may become viable - but only if the firm has the engineering capacity (15+ dedicated technology staff) to maintain what it builds.

Common Concerns About White-Label Platforms

“Our clients will know it’s not our technology.” In a properly implemented white-label deployment, clients interact exclusively with the firm’s brand. The login screen, portal, reports, communications, and mobile experience all carry the firm’s identity. UXDA’s 2024 research on wealth management platform design confirms that client trust is driven by consistent brand experience and interface quality, not by who built the underlying technology. The question is not whether clients know - it is whether clients care. They care about portfolio performance, responsive communication, and a professional digital experience.

“We’ll be locked into one vendor.” Lock-in risk is real but manageable. The mitigation is platform architecture: API-first platforms with documented endpoints, standard data formats, and contractual exit provisions protect the firm’s optionality. The red flag is a platform that stores client data in proprietary formats or requires multi-year contracts without termination clauses. Ask the provider: “If we leave in 12 months, how long does data migration take and what format do we receive our data in?”

“White-label platforms are one-size-fits-all.” This was true five years ago. Modern platforms offer modular architectures where firms configure workflows, compliance rules, approval hierarchies, reporting templates, and client portal layouts. The distinction is between monolithic white-label (limited configuration, vendor-driven roadmap) and API-first white-label (deep customization, firm-controlled workflows). Evaluate accordingly.

“What about our proprietary investment process?” White-label platforms handle operational infrastructure: custody integration, order management, compliance, reporting, onboarding. The investment process - portfolio construction, asset allocation models, rebalancing rules, risk frameworks - remains the firm’s intellectual property configured within or alongside the platform. The platform executes the strategy; the strategy belongs to the firm.

How Aerapass Works as a White-Label Wealth Platform

Most white-label wealth platforms do one thing well - portfolio reporting, robo-advisory, or trading infrastructure - and require firms to stitch together separate providers for payments, compliance, card programmes, and client onboarding. Aerapass takes a different approach: a single regulated infrastructure covering the full client lifecycle.

Three things distinguish this model from other white-label options on the market:

Aerapass is the regulated entity, not just the technology provider. The platform holds its own regulatory licenses in six jurisdictions: Hong Kong, Singapore, Switzerland, Australia, Canada, and the United States. Wealth managers operating on the platform benefit from this licensed infrastructure directly rather than obtaining and maintaining their own licenses in each market. Most white-label platforms provide technology that the firm operates under its own regulatory framework - Aerapass provides the regulatory framework itself.

Wealth management, payments, trading, and card issuance on a single platform. Where most providers specialise in one vertical - a reporting platform here, a payments rail there, a card issuer somewhere else - Aerapass combines portfolio management, global payments, multi-asset exchange (traditional securities, FX, commodities, precious metals, and digital assets), card issuance, and customer management under one integration. This reduces the middleware complexity and vendor management overhead that comes with assembling a multi-provider stack.

Transaction-based pricing aligned to business volume. Rather than subscription fees, AUM-based charges, or fixed licensing costs - the pricing models used by most white-label providers - Aerapass uses transaction-based pricing that scales with the firm’s actual business activity. The firm pays for what it uses, not what it might use.

For wealth managers and family offices, the platform provides:

- Portfolio management and reporting with real-time multi-asset views, consolidated multi-custodian reporting, and downloadable client-branded statements

- Digital client onboarding with integrated KYC, AML screening, PEP and sanctions checks, and configurable approval workflows

- Multi-asset trading across traditional securities, FX, commodities, precious metals, and digital assets on a single platform

- White-label deployment with the firm’s brand, domain, and client experience from day one

The operational evidence: CRJ Capital Partners selected Aerapass as their technology platform, moving from selection to operational deployment in weeks rather than the 12-18 months a custom build would have required. The firm retained full control of its investment strategy and client relationships while Aerapass provided the regulated infrastructure underneath.

$14.9B+ in assets under administration, 100,000+ users across 120+ countries, and 99.9% platform uptime.

Frequently Asked Questions

What is a white-label wealth management platform?

A white-label wealth management platform is technology infrastructure built and maintained by a platform provider but operated by a wealth management firm under its own brand. The firm’s clients see only the firm’s name, logo, and domain. The platform provides portfolio management, trading, compliance, reporting, and client onboarding capabilities without the firm building or maintaining the underlying technology.

How much does a white-label wealth management platform cost?

White-label platform pricing varies by provider - some use subscription fees, others AUM-based pricing, and others transaction-based models. All are significantly less than custom development at $2M-$5M+ over three years. The cost advantage widens with multi-jurisdiction requirements: each new market adds $100,000-$300,000 to custom build costs, while white-label providers absorb multi-jurisdiction compliance into their platform. Pricing varies by firm size and operational complexity - request a tailored analysis from the platform provider.

How long does it take to deploy a white-label wealth platform?

Deployment timelines range from 2-8 weeks for fully hosted models to 8-12 weeks for hybrid deployments with custom integrations. This compares to 12-18 months for a custom-built platform to reach minimum viable product. The primary variables are the complexity of existing system integrations and the depth of brand customization required.

What is the difference between white-label and SaaS wealth management software?

White-label platforms provide the firm complete brand ownership - clients never see the platform provider’s identity. SaaS wealth management software is a shared product where the vendor’s branding, interface patterns, and workflow assumptions are visible to end users. White-label platforms also typically offer deeper customization through APIs, while SaaS products limit configuration to the vendor’s standard options.

Can a white-label platform support digital assets and tokenized securities?

Leading white-label platforms now support traditional securities, FX, commodities, precious metals, and digital assets on a single infrastructure. The critical evaluation point is whether digital asset support is native to the platform architecture or bolted on as an integration. Native multi-asset platforms handle custody, trading, and reporting for all asset classes through a unified system. Bolt-on integrations create reconciliation complexity and reporting gaps.

How do I avoid vendor lock-in with a white-label platform?

Three contractual and architectural requirements mitigate lock-in risk: (1) API-first architecture with documented, versioned endpoints ensures your integration layer is portable, (2) data portability provisions guarantee that client data, transaction history, and compliance records are exportable in standard formats at any time, and (3) contractual exit strategies with defined transition timelines and support obligations. Under DORA, exit strategy provisions are legally required for EU-regulated firms.

Is a white-label platform suitable for small wealth management firms?

White-label platforms are particularly well-suited for firms managing under $5 billion in AUA. At this scale, the economics of custom development are prohibitive - the engineering team required to build and maintain a platform (8-15 engineers) would consume a disproportionate share of revenue. White-label deployment gives small and mid-size firms access to enterprise-grade capabilities - multi-jurisdiction compliance, multi-asset support, institutional reporting - at a fraction of the cost.

Ready to see what a white-label wealth platform looks like? Book a demo to discuss your firm’s requirements, deployment model, and how Aerapass fits your client experience strategy.

The content on this page is produced by Aerapass for general informational purposes only and does not constitute financial advice, investment advice, or any other form of professional advice. Aerapass is a technology platform provider serving financial institutions, wealth managers, and fintech companies. Before making any financial decision, you should consult with a qualified, licensed financial advisor who can take your individual objectives and circumstances into account.