Helping SME with their working capital needs - Trade Finance

Key Takeaways

- The global trade finance gap remains at $2.5 trillion according to the ADB’s 2025 survey - unchanged since 2022.

- Nearly 60% of trade finance rejections come from small businesses, though SME rejection rates (41%) are converging with corporate rates (40%).

- Digital trade platforms could unlock $9 trillion in additional global trade by 2030 through improved SME access.

- Over 80% of banks now report dedicated strategies for supporting SME trade finance.

- Supply chain finance and invoice-backed lending are the fastest-growing digital trade finance segments.

What Is Trade Finance and How Does It Help Small Businesses?

Trade finance is a set of financial instruments - letters of credit, guarantees, invoice financing, and supply chain finance - that enable businesses to conduct international trade by managing the payment and risk gap between buyer and seller. For small businesses, trade finance bridges a critical timing problem: exporters need payment before shipping, importers need goods before paying, and neither party has sufficient trust or capital to absorb the risk alone. Trade finance providers (banks, funds, and digital platforms) step in to guarantee or advance funds, enabling transactions that would otherwise not occur.

Small and medium-sized enterprises continue to face a structural disadvantage in accessing trade finance. Despite representing the majority of global trade activity, SMEs are disproportionately rejected by traditional lenders due to stringent collateral requirements, limited credit histories, and the perceived complexity of underwriting smaller cross-border transactions.

The scale of this problem is well documented. The Asian Development Bank’s latest Global Trade Finance Gap Survey confirms the gap remains at $2.5 trillion in 2025 - one of the most consequential bottlenecks in the global economy.

SME Trade Finance Gap by Region

| Region | Estimated Gap | SME Rejection Rate | Digital Penetration | Key Challenge | Source |

|---|---|---|---|---|---|

| Asia-Pacific | ~$1.1T | 45% | Moderate - growing | Documentation complexity, KYC costs | ADB 2025 |

| Africa | ~$130B | 55%+ | Low | Lack of credit data, correspondent banking decline | AfDB |

| Latin America | ~$200B | 50% | Low-moderate | Currency volatility, political risk | IDB |

| Europe | ~$400B | 35% | High | Regulatory compliance costs for small cross-border trades | EBF |

| Middle East | ~$120B | 40% | Moderate | Concentration risk, trade route disruption | IFC |

Sources: ADB Global Trade Finance Gap Survey 2025, regional development bank estimates. Gap figures are approximations based on survey data and regional trade volumes.

Why Traditional Trade Finance Fails SMEs

The trade finance rejection pattern reveals a structural problem, not a credit quality problem. Banks reject SME applications primarily because the cost of underwriting a $50,000 letter of credit is nearly identical to underwriting a $5 million one, but the revenue is a fraction. Manual document checking, physical bill-of-lading verification, and multi-party correspondent banking chains make small-ticket trade finance economically unviable for traditional banks.

The result: SMEs either forgo international trade opportunities, accept unfavourable payment terms (open account with 60-90 day delays), or turn to expensive informal financing. Each outcome constrains growth and reduces their participation in global supply chains.

How Digital Platforms Are Closing the Gap

Digitalising trade finance addresses the core economics. When trade documents are electronic, credit assessment is automated, and settlement is real-time, the cost of processing a small transaction drops dramatically.

Supply chain finance. Platforms that connect buyers, sellers, and liquidity providers enable early payment to suppliers based on confirmed invoices, providing immediate liquidity without requiring SMEs to take on additional debt. The buyer’s creditworthiness backs the financing, not the SME’s balance sheet.

Digital trade marketplaces. Creating a marketplace where businesses can access a wide range of trade finance providers - including funds and institutional investors - expands access beyond traditional bank financing. SMEs submit funding requests and receive multiple offers from different providers, introducing competition that improves pricing and terms.

Automated credit assessment. State-of-the-art credit assessment models analyse financial statements, transaction history, and alternative data sources to evaluate creditworthiness. This streamlined underwriting process reduces manual effort and enables quicker, more accurate decisions. Risks including operational risk, fraud risk, AML/CTF risk, transport risk, exchange risk, and political risk are identified and managed through platform-level controls.

Cross-border payment solutions. Digital payment platforms and blockchain-based settlement simplify international trade transactions, reducing reliance on traditional correspondent banking networks. Faster settlement means working capital is released sooner, directly improving cash conversion cycles for SMEs.

|  |

|---|

The $9 Trillion Opportunity

The potential is substantial. Industry analysis suggests digital trade platforms could unlock $9 trillion in additional global trade by 2030 through improved access and efficiency. The mechanisms are straightforward:

- Transparent electronic records improve SME creditworthiness without relying solely on collateral

- Standardised digital data through frameworks like the WTO Trade Facilitation Agreement enables SMEs to integrate into global value chains

- Invoice tokenisation - converting confirmed receivables into tradeable digital assets - creates liquidity from previously illiquid working capital

The ADB survey offers one encouraging signal: for the first time, SME rejection rates (41%) have converged with large and mid-cap corporate rejection rates (40%). Over 80% of banks now report dedicated strategies for supporting SME trade finance. The gap is recognised; the infrastructure to close it is being built.

Explore trade finance and working capital solutions on Aerapass

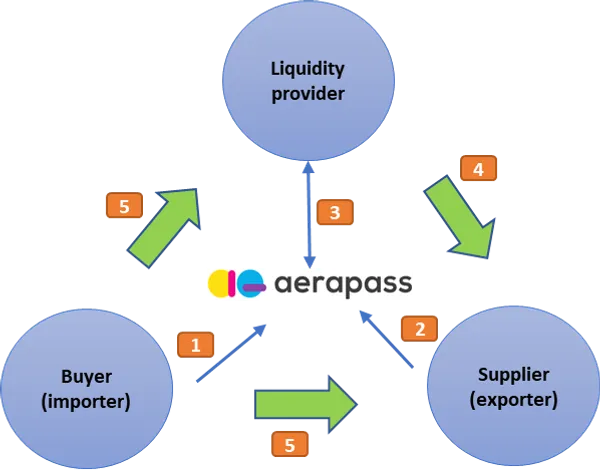

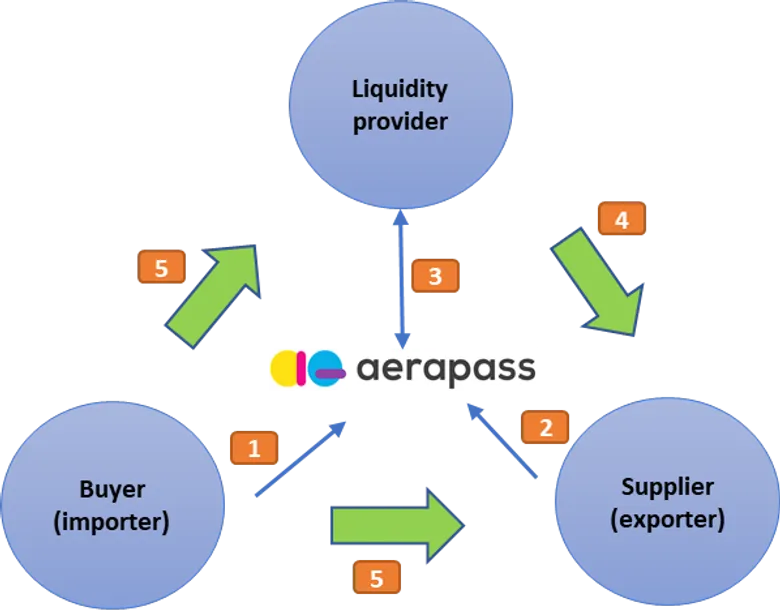

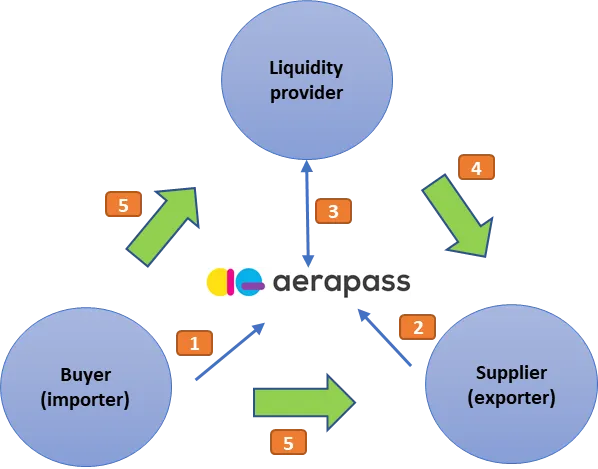

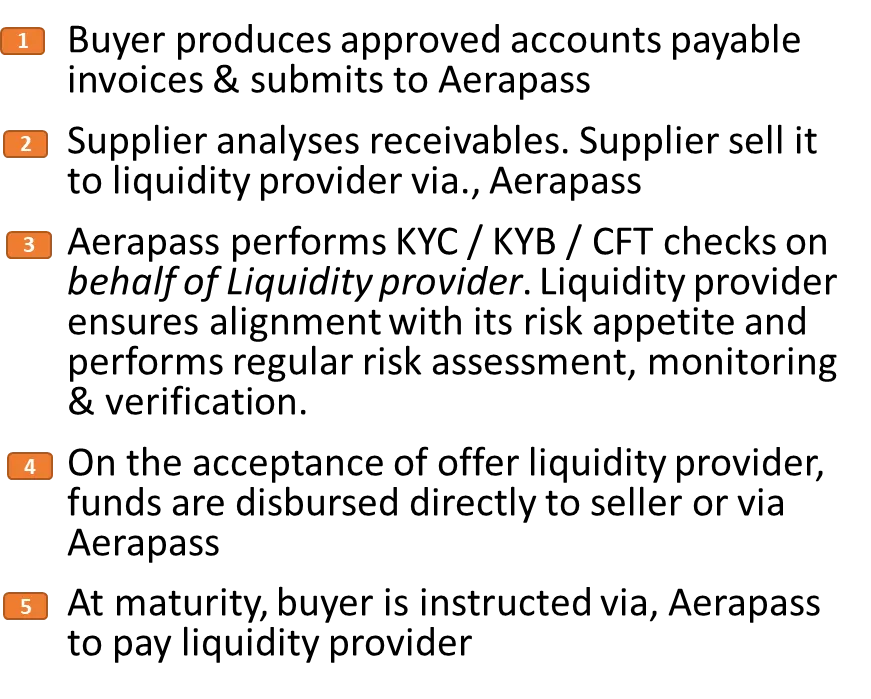

What Aerapass Enables

Aerapass’s digital platform connects buyers, sellers, and liquidity providers in a streamlined ecosystem for trade finance. The platform digitises the trade finance process - document submission, financing applications, and counterparty communication happen online, enhancing efficiency, reducing paperwork, and enabling real-time tracking and transparency.

Specific motivations for factoring and supply chain finance vary by business circumstance. Aerapass recognises these varying needs and provides flexible solutions designed to streamline trade operations across currencies, jurisdictions, and financing structures.

Frequently Asked Questions

How Can SMEs Access Trade Finance Without a Bank?

Digital trade finance platforms have opened alternatives beyond traditional bank channels. Platforms like Centrifuge and Goldfinch (ICC Banking Commission tracks adoption across 250+ banks) enable SMEs to tokenise invoices and receivables, accessing liquidity from institutional investors and DeFi protocols. Supply chain finance programmes allow suppliers to receive early payment based on their buyer’s creditworthiness rather than their own balance sheet. Invoice factoring marketplaces enable SMEs to submit funding requests and receive competing offers from multiple providers. The ADB’s 2025 survey found that over 80% of banks now report dedicated SME trade finance strategies, and for the first time, SME rejection rates (41%) have converged with large corporate rates (40%) - signalling that the access gap, while still significant at $2.5 trillion, is narrowing.

Explore Trade Finance Solutions

Fintech and Neobanking Solutions

Aerapass: Boosting Efficiency and Growth for SMEs

The content on this page is produced by Aerapass for general informational purposes only and does not constitute financial advice, investment advice, or any other form of professional advice. Aerapass is a technology platform provider serving financial institutions, wealth managers, and fintech companies. Before making any financial decision, you should consult with a qualified, licensed financial advisor who can take your individual objectives and circumstances into account.